Get cash-ready for small, urgent expenses—without overcomplicating borrowing

When a sudden bill, family need, repair, travel expense, or medical cost shows up, you may not want a large loan. You may only need a smaller amount, a simple digital journey, and clarity before you commit. That is where a home credit mini cash loan can help you think practically about short-term cash needs.

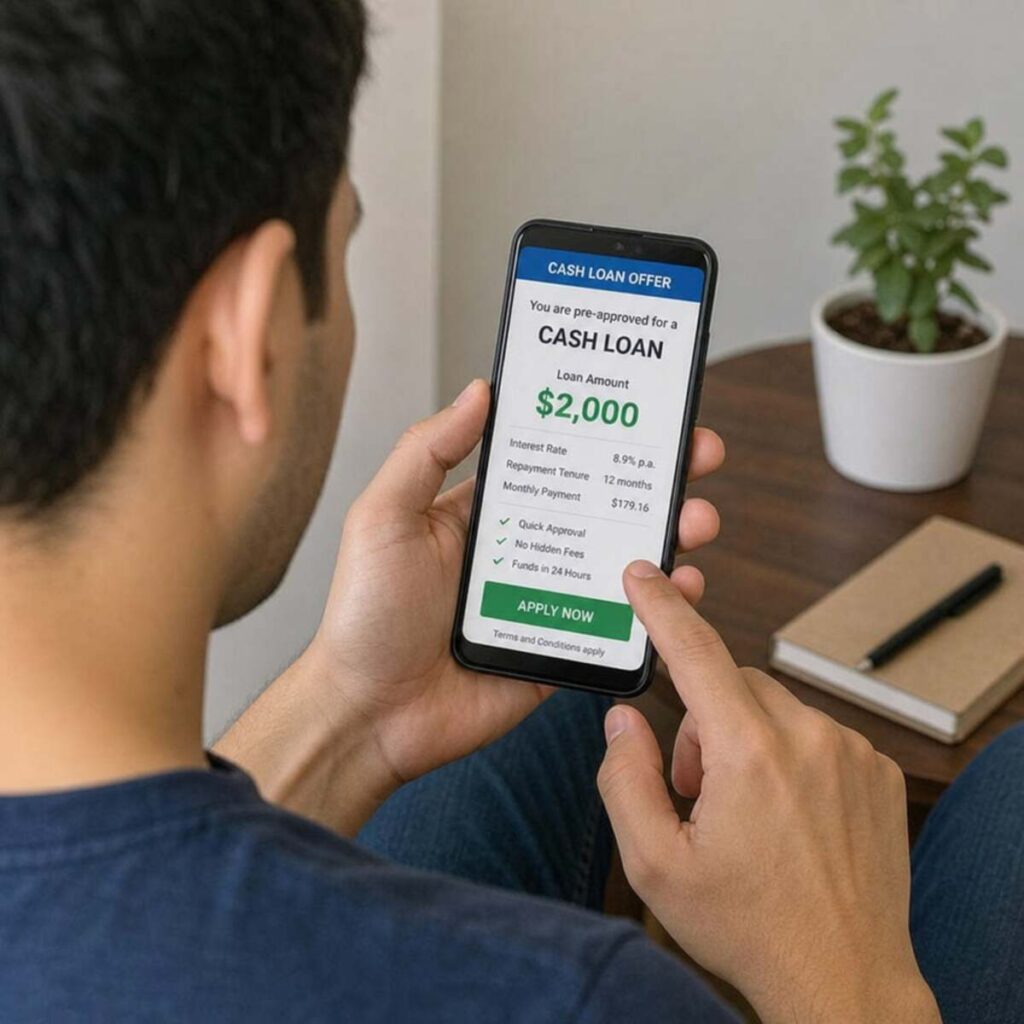

Home Credit India’s own educational content describes a mini cash loan as a short-term loan for a relatively small amount, built for people who need quicker access to funds with minimal documentation. The same official content emphasizes flexibility of use, minimal documentation, and quicker loan decisions as key benefits of this kind of borrowing. (homecredit.co.in)

Ready to check what you may be eligible for?

CTA: Check your offer on the official Home Credit app or website

CTA: Review loan amount, charges, tenure, EMI, and terms before applying

A quick cash loan should make life easier—not heavier

A quick cash loan is useful only when it solves the immediate problem without creating a larger one later. Good borrowing is not just about speed. It is about understanding the amount you need, the EMI you can manage, the total cost you will pay, and the repayment dates you must honor.

For people searching for homecredit.co.in mini cash loan, the intent is usually clear:

- You want to know whether Home Credit offers a small cash loan.

- You want to understand the benefits before applying.

- You want eligibility details in plain language.

- You want to know the documents required.

- You want a simple process, preferably digital.

- You want reassurance that fees, charges, and repayment terms are visible before acceptance.

- You want to avoid scams, fake apps, and unofficial loan agents.

This page is designed to answer those needs in a clear, compliance-friendly way.

Why consider a Home Credit mini cash loan?

A small cash loan can be a practical option when you need funds for a specific, short-term requirement and do not want to borrow more than necessary. Instead of stretching your credit card, disturbing savings, or borrowing informally from friends and family, you can check whether a digital loan offer is available to you.

Home Credit India’s broader personal loan information states that eligible existing customers can check pre-approved loan offers on the Home Credit app and complete the application process directly within the app. The official personal loan page also notes that Home Credit’s personal loan offering is for existing Home Credit customers. (homecredit.co.in)

That matters because a reliable loan journey should give you three things before you proceed:

- Visibility: You should be able to see the applicable offer details.

- Choice: You should decide whether the amount, EMI, tenure, and charges suit your budget.

- Control: You should apply only if the repayment plan is comfortable.

The biggest benefits at a glance

1. Smaller borrowing for smaller needs

Not every expense calls for a large personal loan. Sometimes the need is limited: a repair, a utility bill gap, a medicine purchase, a short travel requirement, or a family emergency. A mini cash loan is built around the idea of borrowing only what is needed for a near-term purpose.

Borrowing smaller can help you stay disciplined. It can also make it easier to plan repayment, provided the EMI fits your monthly budget.

2. A digital-first experience

People searching for an instant cash loan usually want convenience. They do not want multiple branch visits, long queues, or repeated paperwork. Home Credit’s personal loan page says eligible existing customers can check pre-approved offers in the app and complete the application process there. (homecredit.co.in)

A digital journey can help you move from interest to decision faster, but remember: approval, amount, tenure, charges, and disbursal depend on eligibility, policy checks, successful verification, and the terms shown to you.

3. Minimal documentation

Home Credit’s official personal loan page lists PAN as mandatory identity proof and accepts one valid address proof from options such as Aadhaar Card, Voter ID, Driving License, Passport, Government House Allotment Letter, or Property Tax Receipt. It also states that Home Credit may request additional documents if required. (homecredit.co.in)

This is useful because the right documents can reduce friction in the application journey. Before you apply, keep your ID proof, address proof, active bank account details, and mobile number ready.

4. No collateral for eligible personal loan offers

Home Credit’s personal loan page describes its online personal loan as a no-collateral personal loan, meaning you do not need to pledge an asset for that loan type. (homecredit.co.in)

That can be helpful if your requirement is immediate and you do not want to secure the loan against property, gold, or other assets. Still, unsecured loans must be repaid responsibly. Missing EMIs can lead to late payment charges and may affect your credit profile.

5. Flexible use for practical expenses

Home Credit’s mini cash loan educational content says mini cash loans are multipurpose and can be used for different needs such as travel expenses, medical expenses, or house and car improvements. (homecredit.co.in)

That flexibility can be valuable. You decide where the funds are needed most, as long as the loan is used responsibly and in line with applicable terms.

6. Clearer decision-making before you commit

A good loan decision is never based on the word instant alone. It is based on clear numbers. Before accepting any loan offer, review:

- Loan amount

- EMI amount

- Tenure

- Processing fee

- APR or interest rate

- Late payment charges

- Foreclosure terms, if applicable

- Value-added services, if any

- Total repayment amount

- Due date and repayment method

The official Home Credit eligibility page lists personal loan ranges and charges for existing customers, including loan amount, loan term, processing fee, APR range, late payment charges, and foreclosure-related information. Always check the latest offer shown to you at the time of application, because terms may vary by product, profile, and policy. (homecredit.co.in)

Who is this kind of loan best suited for?

A home credit mini cash loan may be suitable if you want a smaller cash cushion and can repay it without straining your monthly budget.

It may fit you if:

- You have a genuine short-term cash requirement.

- You prefer a digital loan application experience.

- You are an existing Home Credit customer or have an eligible offer.

- You can comfortably repay the EMI on time.

- You understand the cost of borrowing before accepting.

- You want to avoid borrowing more than required.

- You have valid KYC documents and an active bank account.

It may not be suitable if:

- You are borrowing to repay another overdue loan without a repayment plan.

- You are unsure whether you can pay the EMI on time.

- You have not reviewed the charges.

- You need long-term debt restructuring rather than short-term funds.

- You are applying through an unofficial app, agent, or link.

- You feel pressured to accept a loan without reading the terms.

The right loan is not the fastest loan. The right loan is the one you can repay with confidence.

Check your eligibility before you apply

Eligibility can vary by product, internal policy, credit assessment, income, repayment history, and the offer available to you. Still, Home Credit’s official personal loan information gives useful guidance for existing customers.

For personal loans, Home Credit’s eligibility information states that applicants should be Indian citizens above 21 and up to 60 years of age, have valid ID and current address proof, be employed, self-employed, or a pensioner, maintain an active bank account, ensure a minimum 90-day gap between Home Credit loan applications, meet household income criteria, and be existing Home Credit customers with a qualifying prior Home Credit product. (homecredit.co.in)

Use this as a readiness checklist:

- You are an Indian citizen.

- You fall within the applicable age range for the product.

- You have valid identity proof.

- You have valid current address proof.

- You have an active bank account.

- You have a stable source of income or pension.

- You meet the gap requirement between loan applications, if applicable.

- You are an existing Home Credit customer, if the offer requires it.

- You can verify your details digitally or through the required process.

CTA: Check eligibility on official Home Credit channels

Documents to keep ready

Documentation is where many loan applications slow down. Keep your documents ready before you begin so you can complete the process with fewer interruptions.

Based on Home Credit’s official personal loan page, PAN is mandatory as identity proof, and one address proof can be selected from listed options such as Aadhaar Card, Voter ID, Driving License, Passport, Government House Allotment Letter, or Property Tax Receipt. Home Credit may ask for additional documents if required. (homecredit.co.in)

Before applying, prepare:

- PAN card

- Current address proof

- Active bank account details

- Registered mobile number

- Income-related details, if requested

- Any additional document requested during verification

Do not upload documents to unofficial apps or unknown links. Use only the official Home Credit app, official website, or verified support channels.

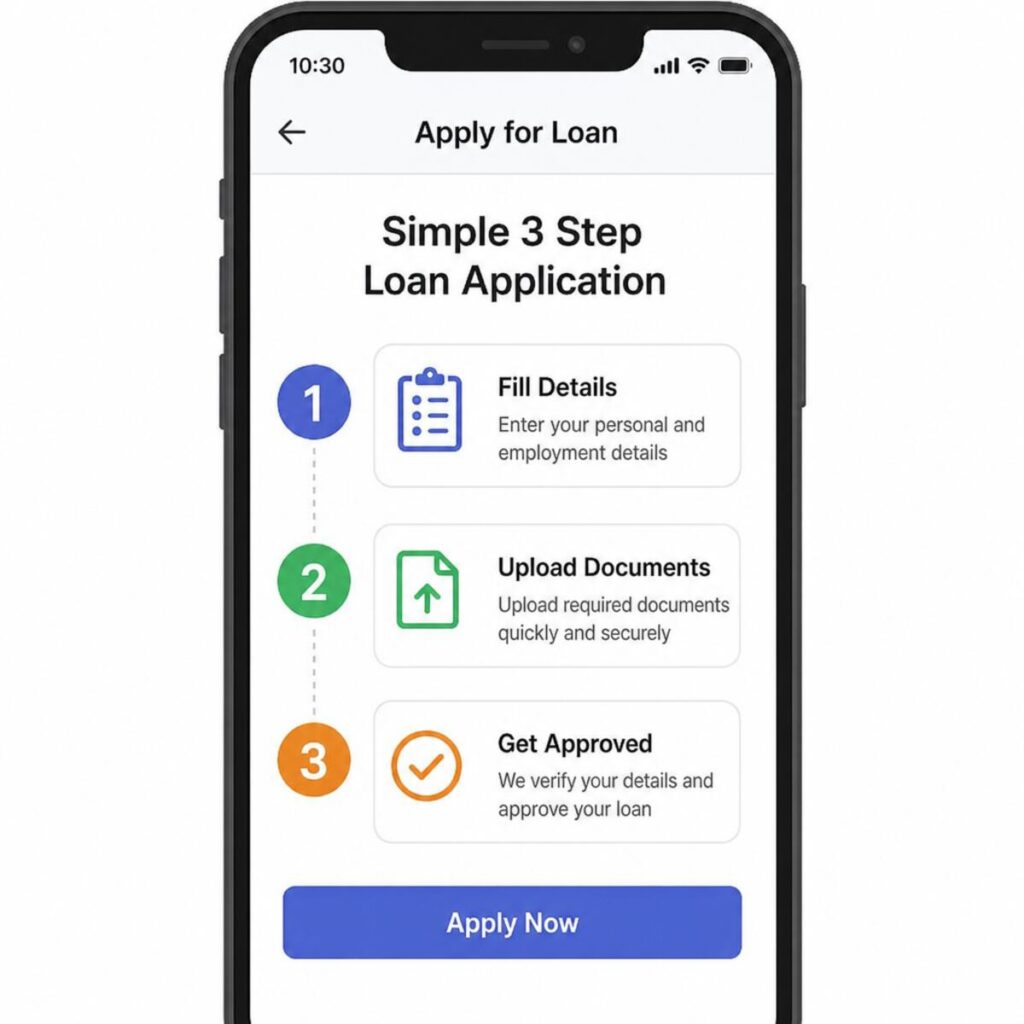

How the application process usually works

A smooth loan process is not magic. It is a sequence of checks. While the exact journey may vary, a digital loan process commonly follows these steps.

Step 1: Start with the official channel

Open the official Home Credit app or website. Avoid clicking unknown loan links received through messages, social media, or unofficial agents.

Step 2: Check available offers

If you are eligible, you may see an available offer. Home Credit’s personal loan FAQ says existing customers can check pre-approved loan offers on the Home Credit app and complete the application process directly within the app. (homecredit.co.in)

Step 3: Choose an amount and tenure carefully

Select only what you need. A larger loan may feel helpful today, but it also means a larger repayment obligation. Choose a tenure that balances EMI affordability with total borrowing cost.

Step 4: Review charges and repayment terms

Before you continue, review the processing fee, APR or interest rate, EMI, total repayment amount, late payment charges, and any value-added services. Home Credit’s official information states that processing fees and APR ranges apply to personal loans, and late payment charges are levied when EMIs are not paid by the due date. (homecredit.co.in)

Step 5: Complete verification

Submit the required documents and details. Verification may include KYC checks, bank details, income-related checks, or other policy requirements.

Step 6: Set up repayment

Repayment setup is important. Home Credit’s personal loan FAQ notes that once a loan is approved, customers can check status through the app, and the loan amount is typically transferred to the bank account within five working days after successful Auto Debit setup. (homecredit.co.in)

Step 7: Track your loan and pay on time

Once the loan is active, track due dates, EMI amount, and repayment status. Paying on time helps you avoid late payment charges and maintain healthier credit behavior.

What makes it a better choice than informal borrowing?

Borrowing from friends, family, local moneylenders, or informal sources can feel easy in the moment. But informal borrowing can create discomfort, unclear terms, and pressure.

A formal digital loan journey can offer:

- Written terms

- A defined EMI schedule

- Visible charges

- A documented repayment process

- Customer support channels

- App-based status tracking

- A structured way to close the loan

That structure helps you make a more informed decision. It also creates accountability. You know what you owe, when you owe it, and how to repay.

Use cases: when a mini cash loan can help

Medical and wellness expenses

A sudden consultation, diagnostic test, medicine purchase, or small treatment cost can create a temporary cash gap. A small loan may help bridge that gap if you can repay comfortably.

Home repairs

Plumbing issues, appliance repairs, wiring work, or urgent maintenance often cannot wait. A quick cash loan may help you manage the expense without delaying essential repairs.

Travel requirements

Emergency travel, family visits, or last-minute work travel can create unplanned expenses. A smaller loan can help cover tickets, fuel, or accommodation if your repayment plan is clear.

Education and learning needs

Exam fees, course materials, online classes, or device-related costs can sometimes need immediate payment. A small loan may help when the expense is important and time-sensitive.

Family commitments

Small ceremonies, family support, or urgent household needs can require extra cash. Borrow only what is needed and only when repayment is manageable.

Income timing gaps

Sometimes the expense arrives before salary, business payment, pension, or receivable. A short-term loan can bridge the timing gap, but only if the upcoming income is reliable.

Responsible borrowing: the guru rule

The Writing Guru rule for loans is simple: borrow with eyes open, not emotions high.

Before you apply for any instant cash loan, ask yourself five questions:

- Do I really need this loan now?

- Is the amount limited to the actual need?

- Can I pay the EMI without missing essentials?

- Have I checked all charges?

- Do I understand what happens if I pay late?

If the answer is yes, you are closer to a responsible decision. If the answer is no, pause. A loan should support your life, not tighten it.

How to calculate affordability before applying

A loan may look affordable when viewed only by amount. The real test is EMI.

Use this simple affordability method:

- Write your monthly income.

- Subtract rent, groceries, school fees, utilities, transport, insurance, and existing EMIs.

- Keep an emergency buffer.

- See what remains.

- Choose an EMI that fits comfortably within that remaining amount.

Do not assume that future income will solve today’s EMI unless that income is certain. If you are self-employed or have irregular cash flow, choose extra caution.

The difference between quick approval and guaranteed approval

Many people search for instant cash loan expecting guaranteed approval. That is not how responsible lending works.

A lender may offer a digital journey and quick decisions, but approval still depends on verification, eligibility, internal policies, repayment history, credit checks, document checks, and the offer available to you.

So when you see words like instant, quick, or digital, read them correctly:

- Instant does not mean everyone is approved.

- Quick does not mean charges are zero.

- Pre-approved does not mean final disbursal is automatic.

- Digital does not mean documentation is unnecessary.

- Small loan does not mean repayment discipline is optional.

The best borrower is not the one who applies fastest. The best borrower is the one who understands the commitment.

Trust signals that matter

Trust is essential when borrowing online. Home Credit India Finance Private Limited’s privacy notice identifies Home Credit as a company incorporated under the Companies Act and registered with the Reserve Bank of India to carry on loans and finance business in India. (homecredit.co.in)

Home Credit’s official website also states that it is trusted by more than 2 crore happy customers. (homecredit.co.in)

When evaluating any loan provider, look for these trust signals:

- Official website and app presence

- Clear company name

- Registered lender information

- Transparent fees and charges

- Customer support details

- Written loan agreement

- Secure document submission

- Visible repayment schedule

- No demand for suspicious upfront cash payments

- No pressure to apply through unofficial channels

If anything feels unclear, stop and verify through official support.

Why official channels are non-negotiable

Loan scams often imitate known brands. They may use similar names, fake social media pages, or unofficial apps. A borrower in urgent need can become vulnerable because speed feels more important than verification.

Protect yourself:

- Download the app only from official app stores.

- Visit the official website directly.

- Do not share OTPs with anyone.

- Do not pay processing money to personal accounts.

- Do not upload documents to unknown forms.

- Do not accept loan offers through unverified WhatsApp groups.

- Do not trust agents who promise guaranteed approval.

- Read the loan agreement before accepting.

A genuine quick cash loan should still feel transparent.

What to review before accepting an offer

Before you click accept, slow down for three minutes. Those three minutes can save months of stress.

Review these items carefully:

Loan amount

Is the amount exactly what you need, or are you borrowing extra just because it is available?

EMI

Can you pay the EMI even in a difficult month?

Tenure

A longer tenure may reduce EMI but can increase total cost. A shorter tenure may reduce total cost but increase EMI pressure. Choose balance.

Processing fee

Check whether a processing fee applies and how it affects the amount disbursed or total cost.

APR or interest rate

Look beyond the EMI. The APR or interest rate helps you understand the cost of borrowing.

Late payment charges

Home Credit’s official eligibility page states that late payment charges apply when dues are not paid by the due date. (homecredit.co.in)

Foreclosure terms

If you plan to repay early, check whether foreclosure charges apply and whether any waiver conditions exist.

Value-added services

Home Credit’s personal loan FAQ states that customers may decide whether to opt for value-added services as per their need during the loan application process. (homecredit.co.in)

Only choose additional services if you understand the benefit and cost.

Why a mini cash loan can be better than using all your savings

Savings are important. But if using all your savings leaves you with no buffer, you may become vulnerable to the next emergency. A small loan can sometimes help preserve liquidity while spreading repayment across EMIs.

However, this is not always the best choice. If you have enough savings and no near-term risk, using savings may be cheaper than borrowing. If you do borrow, ensure that the loan cost is worth the convenience.

The smart approach is not loan-first or savings-first. The smart approach is situation-first.

Why it can be better than borrowing too much

A large loan may feel like breathing room, but unused borrowed money can tempt unnecessary spending. A mini cash loan encourages focused borrowing.

Smaller borrowing can help you:

- Solve a defined need

- Keep repayment manageable

- Reduce the risk of over-borrowing

- Maintain discipline

- Close the obligation sooner, depending on terms

The principle is simple: borrow for the need, not for the feeling of extra cash.

When not to take a quick cash loan

A quick loan is not always the right solution. Avoid applying if:

- You are already struggling with existing EMI payments.

- You need the loan for speculative spending.

- You are borrowing because of social pressure.

- You do not understand the charges.

- You are depending on uncertain income to repay.

- You are taking a loan only to delay a deeper financial problem.

- You are not sure the channel is official.

If your debt is already difficult to manage, consider speaking with your lender, reviewing your budget, or seeking qualified financial guidance before taking another loan.

Common myths about instant cash loans

Myth 1: Instant means no checks

False. Responsible lenders verify eligibility, documents, and repayment capacity. A digital process can be faster, but it still involves checks.

Myth 2: Small loans do not affect credit behavior

False. Small loans still require timely repayment. Missed payments can create charges and may affect your credit profile.

Myth 3: Pre-approved means final approval is guaranteed

Not always. A pre-approved offer may still depend on final verification, acceptance of terms, repayment setup, and lender policies.

Myth 4: Lower EMI is always better

Not necessarily. Lower EMI may come with longer tenure and higher total cost. Review both EMI and total repayment.

Myth 5: All loan apps are safe

False. Always use official channels. Avoid unknown apps, links, and agents.

How Home Credit’s process supports better decisions

Home Credit’s official personal loan information emphasizes app-based offer checking for eligible existing customers, minimal documentation, and no collateral for personal loans. (homecredit.co.in)

That type of process can support borrowers in three ways:

- It reduces unnecessary friction.

- It helps users review offer terms digitally.

- It gives eligible customers a structured path to apply.

Still, your decision should be based on affordability. Convenience is valuable, but repayment comfort is essential.

A simple checklist before you apply

Use this checklist before applying for a home credit mini cash loan or any similar quick cash product:

- I am applying through the official Home Credit channel.

- I have checked whether I am eligible.

- I have kept my PAN and address proof ready.

- I know why I need the loan.

- I am not borrowing more than necessary.

- I have checked the EMI.

- I have checked the processing fee.

- I have checked the APR or interest rate.

- I have checked late payment charges.

- I have checked the repayment date.

- I understand the loan agreement.

- I can repay on time without stress.

If you cannot tick all boxes, pause before applying.

Mini cash loan versus personal loan: understand the difference

A mini cash loan is generally understood as a smaller, short-term cash loan for immediate needs. A personal loan may cover a wider loan amount range and longer tenure, depending on eligibility and product terms.

Home Credit’s official personal loan FAQ says the minimum and maximum personal loan amount for existing Home Credit customers is listed as ₹10,000 to ₹4,80,000, with tenure information also provided on the page. (homecredit.co.in)

Because product names, availability, and terms can change, do not assume that every small cash requirement will be covered under the same label. Check the current offer in the Home Credit app or official website and read the product-specific details before applying.

What happens after approval?

After approval, the next steps typically involve repayment setup, status tracking, and disbursal according to the applicable process. Home Credit’s personal loan FAQ states that customers can check loan status through the app after approval and that the loan amount is typically transferred to the bank account within five working days after successful Auto Debit setup. (homecredit.co.in)

Once the loan is active:

- Save your EMI due date.

- Keep enough balance before auto-debit.

- Track repayment confirmation.

- Contact official support if a payment issue occurs.

- Avoid waiting until the due date if you expect a cash flow problem.

A loan is easiest when managed from day one.

How to improve your chances of a smoother application

No one can guarantee approval. But you can reduce avoidable friction.

Keep your details consistent

Your name, mobile number, ID details, address, and bank account details should match the documents you submit.

Maintain repayment discipline

If you are an existing customer, your repayment behavior may matter. Home Credit’s FAQ mentions that top-up availability is based on repayment history and applicable credit policies. (homecredit.co.in)

Avoid multiple rushed applications

Home Credit’s eligibility page mentions a minimum gap of 90 days between two Home Credit loan applications for certain loan products. (homecredit.co.in)

Choose realistic EMIs

Lenders evaluate risk. Borrowers should evaluate comfort. Do not choose an EMI that requires perfect conditions every month.

Use official support if confused

If you do not understand a charge, status, or document request, use official Home Credit support channels before proceeding.

Compliance-friendly borrowing reminders

Financial products require careful decision-making. Please keep these reminders in mind:

- Loan approval is subject to eligibility, verification, lender policy, and offer availability.

- Charges, APR, tenure, and loan amount may vary by customer and product.

- Read the loan agreement before accepting.

- Pay EMIs on time to avoid late payment charges.

- Do not borrow more than you can repay.

- Do not rely on unofficial agents or fake apps.

- This page is for informational and marketing purposes, not personal financial advice.

What makes a good loan landing decision?

A good landing page can explain benefits. But a good borrower must evaluate fit.

Use the Need, Cost, Comfort, Channel method.

Need

Is the expense important, urgent, and specific?

Cost

Have you reviewed the fee, APR, EMI, and total repayment amount?

Comfort

Can you repay even if another small expense comes up next month?

Channel

Are you applying through the official Home Credit app or website?

If all four are clear, you can move forward with more confidence.

Frequently asked questions

What is a Home Credit mini cash loan?

A home credit mini cash loan refers to a smaller cash loan concept associated with short-term financial needs. Home Credit’s educational content describes mini cash loans as short-term loans for relatively small amounts, with benefits such as flexibility of use, minimal documentation, and quicker decisions. Availability and terms should always be checked on official Home Credit channels. (homecredit.co.in)

Is a mini cash loan the same as an instant cash loan?

Not exactly. An instant cash loan usually refers to a fast digital loan experience or quicker decisioning. A mini cash loan usually emphasizes smaller borrowing. In both cases, approval and disbursal depend on eligibility, verification, policies, and successful completion of the required process.

Who can apply?

Eligibility depends on the product and offer. Home Credit’s personal loan eligibility information states that applicants should be existing Home Credit customers and meet criteria such as Indian citizenship, applicable age range, valid ID and address proof, employment or pension status, active bank account, household income criteria, and the required gap between Home Credit applications. (homecredit.co.in)

Do I need to be an existing Home Credit customer?

For Home Credit personal loans, the official FAQ states that you need to be an existing Home Credit customer and can check pre-approved loan offers in the Home Credit app. (homecredit.co.in)

What documents are required?

Home Credit’s personal loan page lists PAN as mandatory identity proof and accepts one address proof from options such as Aadhaar Card, Voter ID, Driving License, Passport, Government House Allotment Letter, or Property Tax Receipt. Additional documents may be requested if required. (homecredit.co.in)

How fast can I get the money?

Do not assume instant disbursal. Home Credit’s personal loan FAQ states that after approval, the loan amount is typically transferred to the bank account within five working days following successful Auto Debit setup. (homecredit.co.in)

Is collateral required?

Home Credit’s personal loan page describes its personal loan as a no-collateral loan. Always confirm the product-specific terms shown to you before accepting an offer. (homecredit.co.in)

Can I use the money for any purpose?

Home Credit’s educational content says mini cash loans are multipurpose and may be used for needs such as travel, medical expenses, and home or car improvements. Use funds responsibly and according to applicable terms. (homecredit.co.in)

Are there processing fees?

Fees can apply. Home Credit’s official eligibility and personal loan information lists processing fee details for personal loans. The exact fee applicable to you should be checked in your current offer before acceptance. (homecredit.co.in)

What happens if I miss an EMI?

Late payment charges may apply if dues are not paid by the due date. Home Credit’s official eligibility page states that late payment charges are levied in case of non-payment by the due date. (homecredit.co.in)

Can I foreclose the loan?

Foreclosure terms depend on the product and offer. Home Credit’s eligibility page lists foreclosure information for personal loans. Review your agreement or contact official support for the terms applicable to your loan. (homecredit.co.in)

Can I get a top-up loan later?

Home Credit’s personal loan FAQ says top-up availability on an existing personal loan is based on repayment history and applicable credit policies, and customers can check eligibility on the app. (homecredit.co.in)

Is approval guaranteed?

No. Approval is subject to eligibility, verification, credit policy, documentation, repayment capacity, and offer availability. Be cautious of anyone promising guaranteed approval.

How do I avoid fake loan offers?

Use only official Home Credit channels, avoid unknown links, never share OTPs, and do not pay money to personal accounts. If unsure, contact Home Credit through official customer support channels.

Should I take a quick cash loan if I already have debt?

Only if you can repay comfortably and the new loan solves a real need. If you are already missing EMIs or borrowing to repay borrowing, pause and reassess before applying.

Your next step: check, compare, decide

A small loan can be useful when it is taken for the right reason, at the right amount, and with a repayment plan y\ou can manage. A quick cash loan should bring order to a temporary cash gap, not uncertainty to your monthly budget.

If you are considering a home credit mini cash loan, start with the official Home Credit app or website. Check whether an offer is available. Review the amount, EMI, tenure, fees, APR, repayment dates, and terms. Ask questions before accepting. Borrow only when the numbers feel clear.

CTA: Check your Home Credit loan offer through official channels

CTA: Review your EMI and charges before you apply

CTA: Borrow only what you need—and repay on time

The final word from the Writing Guru

Money decisions made in panic often become expensive lessons. Money decisions made with clarity become useful tools.

A home credit mini cash loan may help you handle a small, urgent requirement with a structured process and a digital-first experience. But the real benefit appears only when you borrow responsibly, understand the terms, and repay on time.

So do not chase speed alone. Chase clarity.

Check your eligibility. Read the terms. Compare the EMI with your monthly budget. Use official channels. Then decide.

That is how a loan becomes support—not stress.